Column-QE Sceptics Fear Fed Is In A Hole :Mike Dolan

If this month's U.S. banking stress owes at least something to the Federal Reserve's reduction of its mammoth balance sheet, then the central bank may now find itself digging deeper into a hole of its own making.

Long-standing critics of "quantitative easing" (QE) have for more than a decade blamed the central bank policy of bond buying and balance sheet expansion for many of the world's ills - everything from asset bubbles and inequality to the spillover to poorer economies and the recent inflation spike.

Some arguments stack up, many less so.

Defenders cite the periodic need to flexibly fight greater evils of deflation and depression when official interest rates hit zero. Economists who obsess about tightly calibrating the quantity of money in the system balk at QE as a tool.

But the sudden surge in banking stress this month has many reviewing what's still largely a poorly understood process.

Two weeks of turmoil in mid-sized U.S. banks follow just nine months in which the Fed had been winding down its outsize balance sheet that peaked near $9 trillion during the pandemic. This policy reversal, dubbed 'quantitative tightening' (QT), has proceeded alongside the steepest interest rate hikes in decades.

The sudden re-expansion of that balance sheet last week - aimed at emergency bank backstops that shore up their deposits rather than a fresh round of QE per se - raises big questions about whether the Fed balance sheet may now be stuck at these levels even if interest rates rise once again.

To be sure, the four failed banks snared in the crisis to date can be seen as outliers for a variety of reasons related to poor risk management or inadequate or inconsistent oversight and regulation.

But critics had warned for at least six months that QT may have to be cut short precisely because of the lopsided behaviour of banks toward central bank asset purchases and sales.

In a paper presented to the Fed's Jackson Hole conference in August, and updated this week, former International Monetary Fund chief economist and Reserve Bank of India governor Raghuram Rajan and other economists showed how QT would not just be a dollar-for-dollar mirror reversal of the original balance sheet expansion and may leave banks prone to liquidity shocks.

Citing the Fed's experience in 2018 and 2019 in having to set up emergency liquidity windows after its last bout of QT, the paper's main point was that commercial banks match the reserve assets built via QE with liabilities in the form of deposits or lines of credit.

But the brief history of QE shows that when the former shrink, the latter two don't necessarily follow suit and this asymmetry builds up financial stability risks for many weaker banks if deposits get run down and their replacement asset holdings lose market value - even the 'safest' ones.

"Illiquidity episodes may force central banks to slow the process of reserve withdrawal. Financial stability and monetary objectives of central banks could then conflict," concluded Rajan, New York University's Viral Acharya, University of Chicago's Rahul Chauhan and Sascha Steffen at the Frankfurt School of Finance and Management.

Graphic: Fed QT in question?

Graphic: A balance sheet setback for the Fed, ILLIQUIDTY EPISODES

This could become a trap that prevents normalisation of the balance sheet longer term, they said.

"If aggregate liquidity shortages precipitate systemic liquidity stress, then additional liquidity provision by central banks may resolve the problem temporarily but also strengthen the underlying behaviour that led to the shortages in the first place."

Better-measured and more forward-looking liquidity regulations, incentives for longer-duration deposits during QE bouts and rethinking stress tests were all options, they wrote.

The authors cited the relative success of the Bank of England managing to only temporarily halt its QT plans late last year as it was forced to intervene in the bond market to alleviate pension fund stress after a botched British government budget sparked a run on the gilt market in September.

As Kroll chief economist Megan Greene described in a Financial Times op-ed late last month, QE may just be like "Hotel California", where the lyrics of the Eagles song insist "you can check out but you can never leave."

As the Fed meets this week, markets are still less than sure of policy implications of this March bank blow-up. While a majority now see another quarter point rate rise, many will be closely monitoring signals for just how temporary the latest emergency liquidity provisions will prove.

Bank liquidity operations showed the Fed's balance sheet jumped by around $300 billion in the latest week, undoing almost a half of the drop from the peak of $8.965 trillion in April 2022.

And JPMorgan estimates the Fed injected $440 billion in bank reserves, reversing a third of the $1.3 trillion of those reserves that had occurred since the end of 2021.

But as to how the Fed's balance sheet muddle should be interpreted in the overall context of the Fed's monetary policy, economists at Morgan Stanley stressed how different the latest rescues would be for credit to the wider economy.

Fed asset purchases were vastly different to emergency loans in their implication for onward lending.

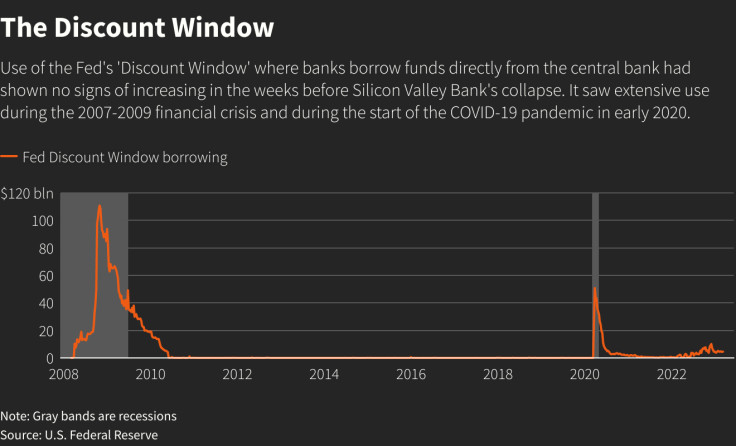

"It won't stop the already tight lending standards across the banking industry from getting even tighter. It also won't prevent the cost of deposits from rising, thereby pressuring net interest margins," Morgan Stanley's Mike Wilson wrote on Sunday. "The risk of a credit crunch has increased materially." Graphic: Odds firm up for a 25 bps Fed rate hike, Graphic: The Discount Window,

The opinions expressed here are those of the author, a columnist for Reuters

(by Mike Dolan, Twitter: @reutersMikeD; Editing by Emelia Sithole-Matarise)

© Copyright Thomson Reuters 2024. All rights reserved.

- MOST POPULAR IN Economy & Markets