Analysis-Debt-laden Italy Looks No Less Vulnerable As Rates Shoot Higher

Debt-laden Italy finds itself in markets' crosshairs again, as the prospect of a collapse in its national unity government coincides with the European Central Bank preparing to deliver its first interest rate rise in 11 years.

Like other indebted euro zone countries, Italy has spent the past few years when cash was cheap and plentiful trying to reduce its vulnerability to rising rates and market panic.

But it is more exposed to increasing borrowing costs than it might appear, according to a Reuters review of its debt profile.

Investors are already fretting about what a possible end to Prime Minister Mario Draghi's government and early elections mean, and how much of a surge in borrowing costs the second most indebted euro zone state can handle.

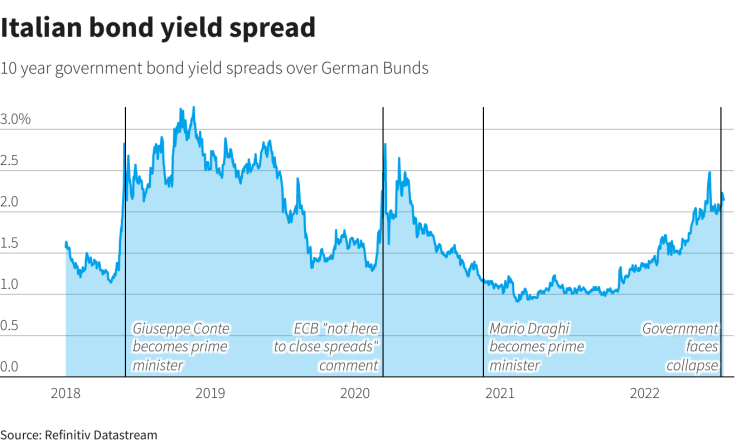

The premium investors' demand to hold Italian bonds over top-rated Germany, a key gauge of market concern, is back above 200 basis points after Draghi last week tendered his resignation. Italy's president rejected that but on Wednesday Draghi demanded unity among his coalition partners if they wanted him to stay in office.

A vote on his speech is expected by 1730 GMT.

GRAPHIC: Italian bond yield spread

For sure, Italy has extended its debt maturities, but by less than Southern European peers and outright debt is higher than it was during the euro zone debt crisis.

"Italy hasn't caught up yet to pre-crises levels and still remains relatively vulnerable," said Janus Henderson portfolio manager Bethany Payne. "Italian debt sustainability is even more prescient due to political instability and the ECB hiking rates," she added.

At around seven years, the average life of Italian debt is lower than it was in 2010 and only marginally higher than in 2012 when the euro zone emerged from a debt crisis.

But the average maturity of Spanish debt has risen to just over eight years from 6.35 years in 2012. In Portugal, it has risen to around seven years from just under six, debt agency data shows.

Italy is also behind on its funding this year, only completing 52% of debt issuance by the end of June versus 68% at the same point last year, Janus Henderson estimates. That means Italy will be borrowing at higher market rates.

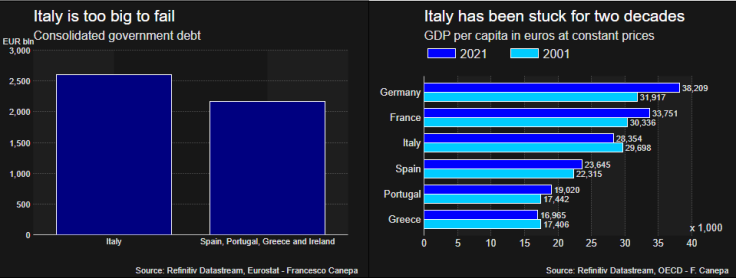

GRAPHIC: Italy is too big to fail and hasn't grown for 20 years

However, Italy's head of debt management, Davide Iacovoni, said last month that the Treasury has the flexibility and financial firepower needed to overcome market volatility.

"Nobody can be comfortable at a time like this, but it is a manageable situation, considering the whole toolbox at our disposal, including 80.2 billion (euros) in liquidity at the end of May," he told a newspaper.

SHORT TILT

On Thursday, the ECB is expected to hike rates to tame record high inflation, and crucially for Italy, to detail a new tool to contain bond market stress.

At 3.31%, Italy's 10-year borrowing costs have surged some 200 bps in 2022, roughly how much they soared in 2011. Investors say 4% is the level where panic sets in. That was breached last month, prompting the ECB to act.

Rising yields increase the cost of servicing Italy's debt. That debt pile rose to a record 2.759 trillion euros in April, according to the Bank of Italy.

Italy remains a very wealthy country - household net financial wealth is an estimated 10 trillion euros - but the problem is refinancing risks as debt comes due.

The country looks vulnerable versus peers because its bond issuance is tilted towards shorter maturities, with 35% of its outstanding debt due by end-2024.

Spain will refinance about 25% of its outstanding debt by end-2024, and Portugal, around 20%.

"Just looking at the seven-year point (in Italy) misses the fact that you have T-Bills and sub-two year debt that is a very large portion of the total stock," said LGIM'S head of rates and inflation strategy Chris Jeffery, who is underweight peripheral euro zone bonds.

While the average maturity of Italy's debt is around seven years, its median maturity - the point when half its outstanding debt comes due - is in around five years, investors note.

That point could be even earlier after accounting for central bank bond purchases, according to some estimates.

Even if debt is not due immediately, rising yields impact banks and borrowing costs for firms and households instantly by "getting into the economy's bloodstream", notes Rabobank's head of rates strategy, Richard McGuire.

"The optimistic notion of a seven-year weighted average maturity of Italian (debt) clearly did nothing to assuage these concerns, hence the ECB needed to step in last month," he said.

© Copyright Thomson Reuters 2024. All rights reserved.

-

McDonald's Extending $5 Meal Deal, Creating McValue Menu

-

South Sudan Probes Shootout At Sacked Spy Chief's Home

-

Pregnant Indiana Mother 'Threw' Her Baby Daughter After She Cried, Police Say

-

Top US Securities Regulator To Exit, Clearing Way For Trump Pick

-

Canada AI Project Hopes To Help Reverse Mass Insect Extinction

-

Aid Groups Express Horror At US Mines For Ukraine

-

As Trump Returns, China Seizes Chance For Climate Mantle

-

Taxing The Richest: What The G20 Decided

-

US Agency Opens Two Probes Into Ford Vehicles Amid Quality Control Concerns

-

Trump-Inspired Campaign Playbook? Polish Presidential Aspirant Vows To Turn Poland Into 'Crypto Haven'