Analysis-Europe's Banks Brace For Bumpy Ride After Cheap Money Decade

Europe's banks, facing a potential economic storm and a rise in borrowing costs for the first time in more than a decade, are set to show their weak spots when they update investors on how their business has fared this year.

They have already had to cope with soaring inflation and rising interest rates, a pincer movement that squeezes borrowers, plus the Ukraine conflict which has rattled Europe's economy, including by constraining its energy supplies.

UBS, Deutsche Bank, Credit Suisse, BNP Paribas and UniCredit could set the tone for investors when they report second-quarter results next week.

On one hand, higher interest rates are good for banks as they can charge more for loans. But they suffer if customers, struggling with rising prices and borrowing costs, cannot repay.

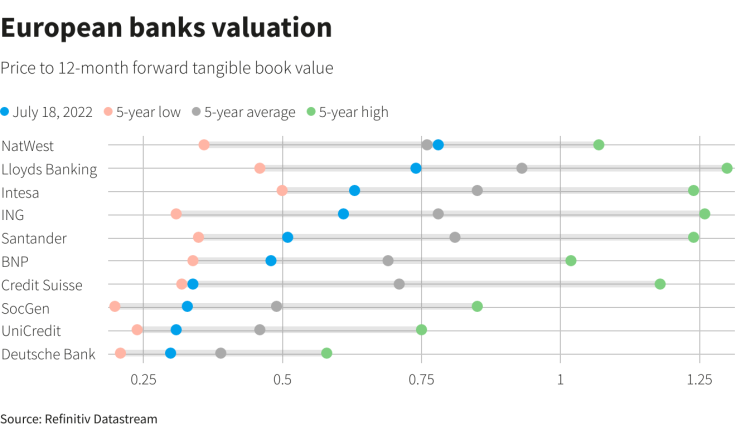

Graphic: European banks valuation-

The difficult economic conditions have put investors in a cautious mood, which means European banks, like their U.S. rivals, will earn less money on deal making and selling investment products.

Within Europe, Germany's banks are at the centre of the storm because the country is particularly dependent on Russian energy and its economy will be hit hard by any supply shortages.

Giles Edwards, an analyst with the ratings agency S&P, said any fears about European banks this year will hinge on how borrowers' keep up loan repayments.

Although he did not expect a big immediate rise in bad loans, he said he was watching for "early warning indicators, signs that there's pressure, a sort of slow squeeze essentially starting to sort of pop a few buttons here and there".

Analysts are also watching developments at Uniper , the German power company that received a state bailout on Friday. [nL8N2Z32QK]

German banks may still have to set aside more for resulting loan losses, said Michael Rohr, an analyst with credit rating agency Moody's.

Over the past two months, analysts have cut profit forecasts for Germany's biggest bank Deutsche Bank, which has emerged from a series of crises, and raised predictions for the amount of bad loan provisions it needs. For Deutsche, the biggest risk is "a severe recession", Rohr said.

Other warning signs are flashing.

Euro zone banks tightened access to credit in the second quarter and will continue to be cautious, a survey by the European Central Bank showed.

And Germany's cooperative banks said they expect a "considerable decline" in profit this year as they brace for credit losses.

Highlighting these worries, euro zone bank stocks have fallen more than 22% year-to-date, underperforming the wider pan-European STOXX 600 index of shares which is down roughly 13%.

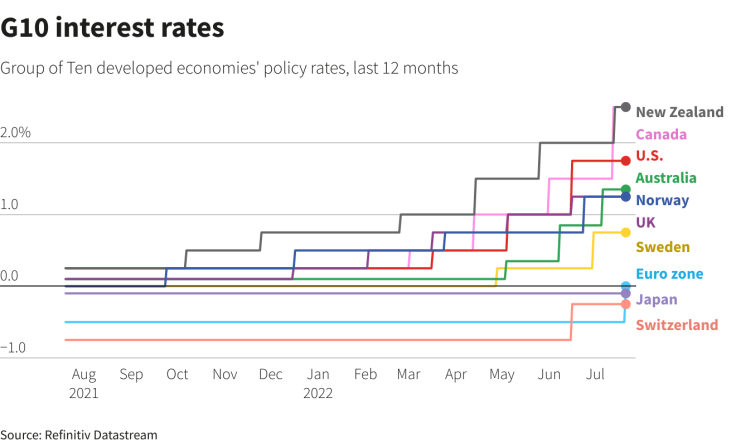

Graphic: G10 interest rates-

'SLOW SQUEEZE'

The ECB, which raised interest rates by a surprise 50 basis points on Thursday to tame runaway prices, has earlier also warned of potential perils, such as an overheated property market.

During the pandemic, governments spent billions to prop up much of the economy, but the ECB has said that this time around they may not be able to.

In Spain, one senior Spanish economic official, who asked not to be named, said banks are generally vulnerable, pointing to a large number of loans under special surveillance for default and the potential lifting of payment moratoriums.

"I don't know what the real impact ... is going to be and ... that worries me," said the official. Santander and BBVA report second-quarter results at the end of the month.

In Italy, gripped by a political crisis, pressure is mounting on the country's government bonds, which also erodes the capital cushions of the banks as the Italian government bonds they hold lose value.

Italy's reliance on Russian gas and the importance of its manufacturing sector, made up mostly of small businesses, increase the chances of a recession.

Almost 300 billion euros (or more than 40%) of Italian corporate loans are guaranteed by the state after banks used emergency measures during the pandemic to refinance existing debts.

While Britain's banks are expected to chalk up solid results, Tom Merry, a banking strategy consultant at Accenture, said he expected an increase in bad loan provisions.

NatWest is expected to swing from releasing 38 million pounds ($45.43 million) worth of cash put aside against potential defaults in its first quarter results, to new impairment charges of 136 million pounds, based on a poll of analysts.

In higher margin investment banking, Europe's banks are likely to see a slump in year-on-year banking fees similar to that reported by U.S. rivals earlier this month, analysts said.

JPMorgan and Morgan Stanley reported investment banking fees fell by more than half compared to a year ago. U.S. merger volumes fell by 29% in the first half of this year, based on Refinitiv data, while they rose 1% in Europe.

Barclays, with its significant U.S. business, may see a performance similar to Wall Street rivals, while banks like HSBC and Standard Chartered, with their Asia focus, could fare better.

($1 = 0.8365 pounds)

(Writing by John O'Donnell; Reporting By Tom Sims in Frankfurt, Jesus Aguado in Madrid, Lucy Raitano, Iain Withers and Lawrence White in London, Valentina Za in Milan and Noor Zainab Hussain in Bengaluru; Editing by Jane Merriman)

© Copyright Thomson Reuters 2024. All rights reserved.

- MOST POPULAR IN Economy & Markets