Analysis-LIBOR Sunset Could Get Stirred Up By Banking Turmoil

A crisis of confidence in global banking and a backlog of uncleared contracts is making an already cumbersome shift to a new set of rates even harder as the end of the LIBOR era approaches, according to industry experts.

Once dubbed the world's most important number, London Interbank Offered Rate or LIBOR, is a rate based on quotes from big banks on how much it would cost to borrow short-term funds from one another. It was discredited when authorities found traders had manipulated it, prompting calls for reform.

It is largely being replaced by risk-free rates (RFRs) compiled by central banks as they are based on actual transactions, including the Federal Reserve's Secured Overnight Financing Rate (SOFR) for instance, making them harder to rig.

Libor has already been scrapped for use in new contracts, with the use of a few remaining dollar-denominated rates in outstanding contracts due to end in June.

"With the transition deadline in sight, LIBOR's grand finale may be more dramatic than previously thought with derivative contracts piling up amid the current banking turmoil," said Glenn Yin, head of research and analysis at AETOS Capital Group.

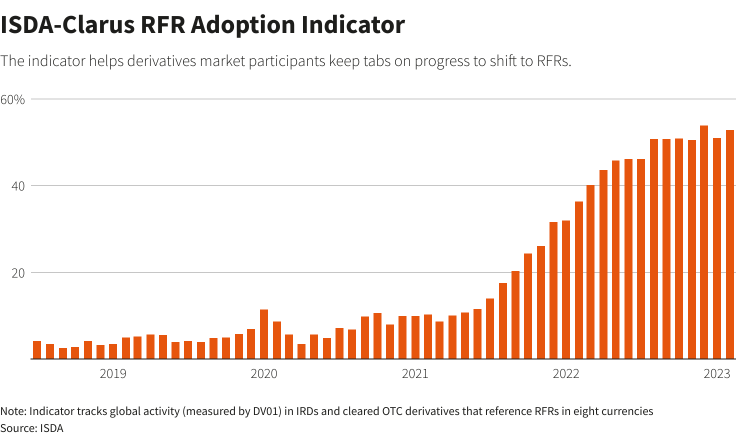

Global trading activity (as measured by DV01) in cleared over-the-counter (OTC) and exchange-traded interest rate derivatives (IRD) that reference RFRs in eight major currencies was at 52.9% in February, according to the ISDA-Clarus RFR Adoption Indicator.

It helps derivatives market participants keep tabs on progress on the shift to RFRs. The indicator was at 4.7% in June 2020 and then surged to 53.9% in Dec 2022, its highest level, before declining slightly in the first two months this year.

DV01 is a gauge of risk that represents the valuation change in a derivative contract resulting from a 1 bp shift in the swaps curve.

(Graphic: ISDA-Clarus RFR Adoption Indicator -

)

"SOFR's slow uptake was already setting the stage for a late rush to amend credit agreements, and I suspect the ongoing challenges in the banking sector will push transition plans back even further," said Matt Orton, chief market strategist at Raymond James Investment Management.

Banks around the world are facing a major upheaval after three U.S. banks collapsed in a week and 167-year old Swiss banking giant Credit Suisse was taken over by UBS in a state-orchestrated rescue to stem broader repercussions in the crisis-laden sector.

"The current turmoil is forcing banks to split their focus and may be diverting resources from the transition," said Gennadiy Goldberg, U.S. interest rate strategist at TD Securities.

"This might make it a bit more difficult for banks to transition on time, but I suspect regulators are highly unlikely to postpone the end date for Libor," Goldberg added.

While plans are in place to convert cleared U.S. dollar LIBOR swaps and eurodollar futures and options into corresponding contracts referencing SOFR before June 30, non-cleared derivatives that continue to reference U.S. dollar LIBOR "may transition via bilateral negotiations," ISDA said earlier this month.

Many contracts will reference SOFR-based fallbacks after that date and the Adjustable Interest Rate (LIBOR) Act will replace U.S. dollar LIBOR in tough legacy contracts that do not have fallbacks and don't provide clearly defined benchmark replacements.

"Only about 15%-20% of outstanding loans are using SOFR and I fully expect to see administrative logjams for borrowers, lenders, lawyers, and bankers," said Orton.

Around 80% of institutional loans and collateralized loan obligations (CLOs) are still tied to LIBOR even as it nears its June 30 end-date, private equity firm KKR & Co Inc said last month. KKR and Co is also a lender, borrower and investor in CLOs.

Libor has been used globally to price trillions of dollars of financial products from mortgages and student loans, to derivatives and credit cards.

"One of the hurdles in the flip to SOFR has been in agreeing to amendments that address credit spread adjustments, and the wild swings in the market will only add to lender reticence to resolve these issues in the near term," said Orton.

© Copyright Thomson Reuters {{Year}}. All rights reserved.

- MOST POPULAR IN Business