Analysis-Safe As Houses? Rising Rates Test Foundations Of Property Boom

In Toronto's far-flung suburbs, just a few months ago a typical three-bedroom house would have fetched 40 offers on bidding night and sold well over the asking price. Now, home-buyers have become hard to find.

"You're not getting the bidding wars anymore," said Tim Keung, chief executive of TimSold Real Estate, a local agency.

"A lot of buyers are... sitting on the sidelines, waiting for this big correction to happen."

They are not alone. A decade-long boom in housing prices from the United States to Europe and Asia is facing its first real test as borrowing costs rise and high inflation eats into households' budgets.

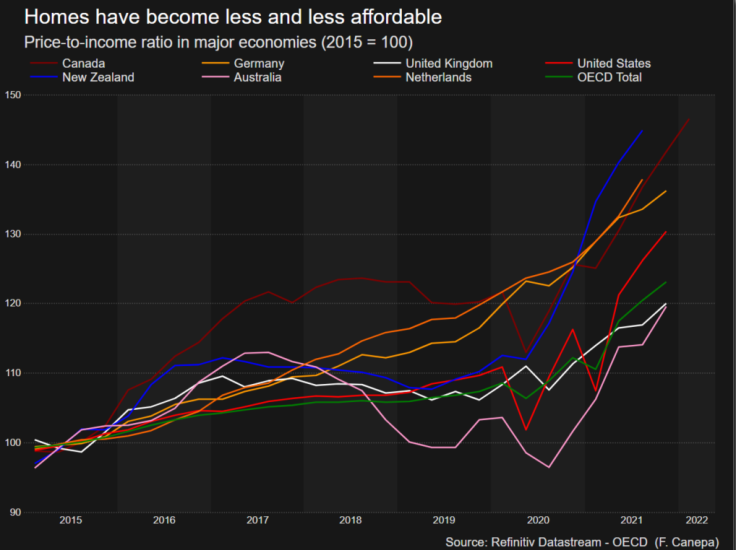

Beyond Toronto, home prices are already falling in some of the places that have seen the biggest appreciation, such as China, New Zealand and parts of Australia.

Growth has slowed in Singapore and South Korea and volumes are dwindling in the United States and Poland.

Lenders and regulators from across the most industrialised nations have warned that inflated home prices may now stagnate or fall - in some cases by as much as a quarter.

While every market is different, they nearly all have one thing in common: a surge in the cost of borrowing as central banks around the world raise interest rates to fight inflation.

The average rate on a 30-year fixed-rate mortgage in the United States, a barometer for the rest of the world, has surged from just 2.7% in late 2020 to 5.5% now, the highest level since 2008, according to the Mortgage Bankers Association.

This is below the levels that prevailed in the 2000s but the sheer pace of change in fixed and variable rates is straining buyers and owners already struggling with a higher cost of living.

This threatens to prick property bubbles that have been financed by cheap credit over the past decade and grew even bigger during the pandemic, when some people saved more and looked for bigger abodes.

"The high real estate prices and rising mortgage rates are increasingly a problem for the affordability of residential property," said Joerg Utecht, chief executive of German mortgage broker Interhyp.

Swiss bank UBS ranks Frankfurt in Germany as the city with the biggest bubble risk, followed by Toronto, Hong Kong and Munich, Germany, based on factors such as the relationship between prices, incomes and rents.

Similarly, German bank LBBW estimates that home prices in Europe's largest economy have risen by 20%-25% more than demand and supply would justify since 2015, meaning they could fall by that much if borrowing costs go back to where they were then.

German borrowers were paying just 1% for a 10-year fixed rate mortgage last year but this has risen to 2.5%, the highest level since 2014, and could well hit 3% by the end of the year, according Interhyp.

Economists polled by Reuters have already started cutting their forecast for home price growth in Germany for the next two years.

(Graphic: Homes have become less and less affordable-

)

FEEL THE HEAT

Homeowners with a variable-rate mortgage are also starting to feel the heat.

In Poland, where such loans are the norm and the central bank has raised rates from 0.1% to 5.25% since October to stem now double-digit inflation, the government is stepping in to help borrowers via payment holidays.

In the northern town of Rotmanka, 31-year-old office worker Maciej Kawka has seen the monthly mortgage payments on his small flat rise by 18% since he took out the mortgage in 2018. He now pays 1,650 zlotys ($384.62) a month. However, he expects payments to increase to 1,800-1,900 zlotys when the latest two central bank hikes are factored in, further pressuring his finances which are also being squeezed by surging energy and food prices.

"Our budget will be much tighter: no holidays, nothing that goes beyond day-to-day life," Kawka, who lives with his wife and daughter, said. "But if (rates) keep rising I don't know what will happen."

Elsewhere, homeowners are locking in current rates, fearing further surges.

Dennis Willeke, a 35-year-old firefighter, has secured a 2.15% fixed rate for the next 10 years on the house where he lives with his wife and two children in the western German town of Neukirchen-Vluyn.

"We have rushed to refinance because I think it will rise still," he said.

In New Zealand, American Lee Stewart and his wife are anxious about a repeat of the 2007-09 property crash, when millions of homes were repossessed in the United States alone and the couple ended up selling theirs at a loss.

Spooked by the rise in rates, which started in New Zealand earlier than in most other countries, Stewart has fixed his own mortgage costs for three years.

"Small changes in that percentage make a big difference... to somebody who has a pretty big loan," the 40-year-old said.

Yet analysts don't expect a repeat of the collapse that started the global financial crisis 15 years ago.

First, the share of variable-rate loans has shrunk to just 10% of all mortgage applications in the United States and 20% of all household debt in the euro zone in just over a decade.

Second, with the notable exception of China, most countries are still facing housing shortages, which are now exacerbated by a lack of labour and materials due in part to the after effects of lockdowns during the pandemic. Those countries include the United States, Germany.

This was seen putting a floor on prices.

But Canada and New Zealand show how fast that can change when higher rates cool demand.

"Right now, if there are 10 things on a buyer's wish list and the house doesn't have eight of them, they're just going to pass," said Brad Goetz, an agent at Canada's Right at Home Realty. "Where prior to this, it was just like, 'Hey, it has four walls and a kitchen and a bathroom. We're good.'"

(Graphic: U.S. mortgages have become much more expensive-

)

($1 = 4.2900 zlotys)

© Copyright Thomson Reuters 2024. All rights reserved.

- MOST POPULAR IN Economy & Markets