Another Mixed Quarter For IBM

International Business Machines' (NYSE:IBM) second-quarter report was the last to not include any contribution from Red Hat. IBM closed its $34 billion acquisition of the open-source software company on July 9. Starting with the third quarter, Red Hat will provide IBM with a revenue boost.

That extra revenue is much needed. IBM's sales tumbled more than expected in the second quarter, driven by currency, an aging mainframe product cycle, and weakness in the global technology services segment. Revenue grew in high-value areas, which helped to push up gross margin and earnings per share, but it wasn't enough to prevent another revenue decline.

High-value growth

IBM reported second-quarter revenue of $19.16 billion, down 4.2% year over year and $40 million below the average analyst estimate. Adjusted for currency, revenue would have only declined by 1.6%.

Cloud revenue, which spans multiple reporting segments, was $19.5 billion over the past 12 months, up 5% year over year, and up 8% adjusting for currency. Some of IBM's hardware revenue is counted as cloud revenue, so a decline in hardware revenue reduced the cloud growth rate.

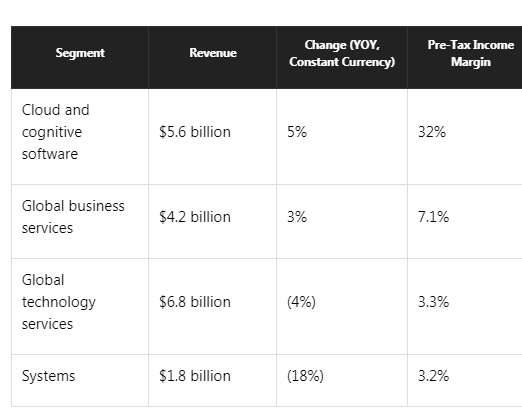

IBM grew revenue in its two higher-margin segments, while revenue sank in its lower-margin segments:

Within the cloud and cognitive software segment, cloud and data platforms revenue jumped 7%, cognitive application revenue rose 5%, and transaction processing platforms revenue increased 4%. Within the global business services segment, growth was led by a 5% increase in consulting revenue.

The decline in systems revenue was due to a 41% drop in mainframe revenue and a 21% drop in storage revenue. The mainframe weakness was expected, given that the last major iteration launched about two years ago. The only part of the system segment that grew was Power systems, which enjoyed a 3% jump in revenue.

On an adjusted basis, gross margin rose 1 percentage point year over year to 47.4%, while pre-tax margin slumped 0.3 percentage points to 16.6%. Adjusted earnings per share rose 3% to $3.17, beating analyst expectations by $0.09. Share buybacks helped the cause by reducing the outstanding share count.

A guidance update is coming

IBM plans to update its full-year guidance to reflect the acquisition of Red Hat on Aug. 2. The company still expects the deal to increase free cash flow in the first year after closing, and to increase adjusted earnings per share by the end of the second year after closing. In 2019, earnings per share are expected to be reduced because of non-cash purchase accounting adjustments related to the deal.

While investors will have to wait for an updated outlook, IBM did reiterate its previous full-year guidance excluding the impact of the Red Hat acquisition. The company still expects to produce adjusted earnings per share of at least $13.90, and free cash flow of approximately $12 billion. The adjusted earnings figure excludes financing costs associated with the Red Hat acquisition, but it doesn't take into account any other Red Hat-related costs or activity.

Acquiring Red Hat was a massive bet on hybrid, multi-cloud computing. "With the completion of our acquisition of Red Hat, we will provide the only true open hybrid multi-cloud platform in the industry, strengthening our leadership position and uniquely helping clients succeed in chapter 2 of their digital reinventions," said IBM CEO Ginni Rometty in prepared remarks included in the company's earnings release.

IBM's cloud revenue growth is slowing, and its overall revenue is in decline. If the Red Hat deal lives up to the company's expectations, it could solve both problems. But that's a big if.

This article originally appeared in the Motley Fool.

Timothy Green owns shares of IBM. The Motley Fool is short shares of IBM and has the following options: short January 2020 $200 puts on IBM, short September 2019 $145 calls on IBM, and long January 2020 $200 calls on IBM. The Motley Fool has a disclosure policy.

- MOST POPULAR IN Business