Business Fights Back As Republican State Lawmakers Push Anti-ESG Agenda

U.S. political battles over corporate sustainability are turning hotter this spring as aggressive Republican statehouse efforts face increasing pushback from businesses and pension funds looking to account for climate change and protect returns.

Dozens of Republican-sponsored bills aim to free fossil fuel companies from climate-driven constraints adopted by some Wall Street firms. Others touch on hot-button environmental, social and governance (ESG) topics like abortion rights and firearms.

Those stances have been adopted by some conservative legislators who say the laws are needed to counter ESG-minded shareholder activists, citing cases like the 2021 investor revolt at Exxon Mobil Corp over climate concerns.

But as the number of the so-called "ESG backlash" bills multiply, the proposed laws have in turn provoked their own reaction from business leaders, legislators and public officials who worry they would hurt returns by cutting off public pension funds from outside investment managers or interfere with executives' obligations to shareholders.

A Reuters review of testimony, previously unreported public documents and interviews with elected leaders, lobbyists and attorneys detail mounting challenges to many pending anti-ESG bills.

The tussles have financial implications for some of the largest investment firms that manage billions of dollars for state pension plans. Wall Street money mangers stand to lose big business or walk away if and when restrictions are placed on public investments, even as they balance pressure from officials in Democratic states.

Lauren Doroghazi, senior vice president at government relations consultant MultiState Associates, said the debates show lawmakers coming to terms with the anti-ESG bills' practical impact.

"There has certainly been a lot of pushback and education about how this might operationally affect some particular industries," she said.

She estimates fewer than a fifth of the anti-ESG ideas and policies originally sought would be passed into law, a share that could still prove significant.

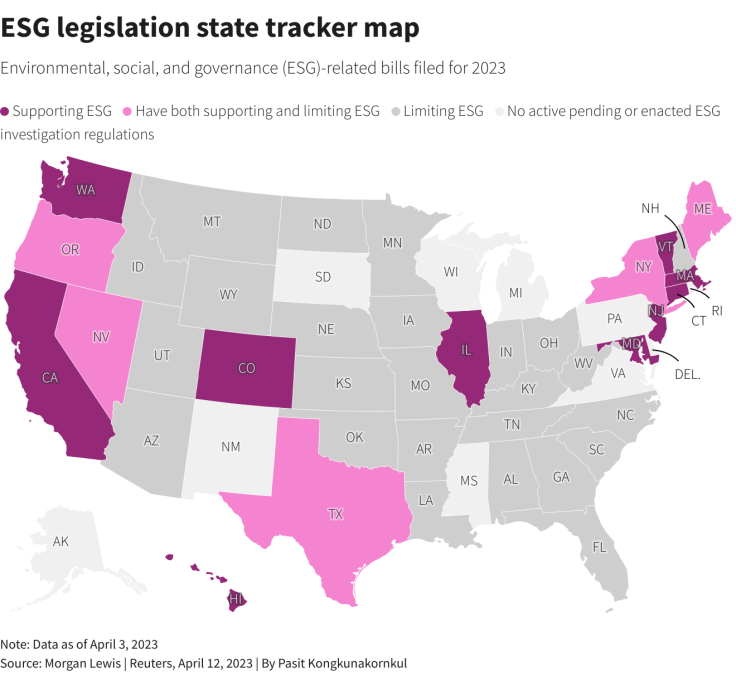

GRAPHIC: ESG legislation state tracker map

"RICHER PUBLIC DIALOGUE"

This year state legislators, chiefly Republicans, have filed roughly 99 bills aimed at restricting the rise of ESG business practices, up from 39 in 2022, according to law firm Morgan Lewis. As of April 3, seven of the bills had been enacted into law, 20 were effectively dead, and 72 were still pending.

One Texas bill would require fund managers working for the state to only seek maximum profits rather than to further social or political goals.

Several public pension systems raised concerns about it, including the largest, the $182 billion Texas Teacher Retirement System (TRS). In a March 24 document, TRS said external managers running some $76 billion of its assets could have run afoul of the proposed legislation.

In response, Sen. Bryan Hughes, a Republican, put forward a narrower version of the bill, leading TRS to remove the estimate about its outside managers in an April 13 document. But two other systems, including the Texas County & District Retirement System (TCDRS), said they remained concerned.

In an April 14 document provided to Reuters under a public records request, a TCDRS official wrote the new language "still creates risks and liabilities that cause concern" and may discourage investment managers from doing business with TCDRS.

It also said the "financial impact is not determinable" but may result in significant lost earnings. TCDRS declined to comment further.

Hughes' proposal was passed by the Texas Senate 25-4 on April 20, but still must be heard by the Texas House in coming weeks.

If passed, it would follow a 2021 Texas law limiting state investments in equity and products of asset managers including BlackRock Inc over their climate change stance.

In a recent interview, BlackRock Chief Financial Officer Martin Small said the conversation about ESG is changing in many states.

"I think there's a better, richer public dialogue happening where people are talking not just about their issues with ESG, but people are also talking about the problems and potential costs that might be incurred by public pension plans as a result of some of these bills," Small said.

SATAN'S WORK

ESG investing debates have taken on national significance as Democratic-aligned shareholder activists clash with Republicans increasingly adopting anti-ESG rhetoric.

Some of the criticism has been harsh. Utah's Republican State Treasurer Marlo Oaks in March referred to ESG governance and to United Nations-backed sustainable development goals as "Satan's plan" when speaking to a meeting of Republicans.

The comparison with Satan was unusual. But Republicans often disparage ESG efforts with references to the global connections of top funds and characterize industry efforts like the Net Zero Asset Managers initiative as radical.

Oaks supported a number of anti-ESG bills signed into law this spring, a spokeswoman said, including one that prohibits public agencies from doing business with companies seen as 'boycotting' industries like fossil fuels.

Utah Bankers Association President Howard Headlee said the new law could have unintended consequences. For instance, if federally-regulated local banks faced new national rules on an issue like climate change disclosures, banks would need special permissions from local officials to keep public business in Utah he said.

"It's a foolish way to structure this," he said.

"ONE BITE AT A TIME"

Democrats have also filed far-reaching bills such as a pair in California to require companies to disclose greenhouse gas emissions and for state pension funds to divest fossil fuel stocks.

Ultimately local politics will determine outcomes. This month in Kansas, legislators softened language in a Republican bill aimed at limiting the use of ESG in investment decisions to address concern it would cost $3.6 billion over 10 years in lower pension system returns.

Another provision excluded from the final legislation would have required registered investment advisors to get extra consent from clients to put them into ESG-type funds.

Bill author Sen. Mike Thompson said the changes were needed to assure final passage. It was passed by both houses of the Kansas legislature on April 6 and will become law unless vetoed by Governor Laura Kelly, who has until April 24 to do so.

A spokesperson for Kelly did not comment on her intentions.

"We think our model may be used in other states who are also struggling to pass this type of bill," Thompson said via e-mail. He added that "Sometimes you must take it one bite at a time."

© Copyright Thomson Reuters 2024. All rights reserved.

- MOST POPULAR IN National