Cyprus' Bailout By The EU And The IMF Is Small Change Compared To What The Other Euro Zone Countries, Including Spain And Greece, Have Received [INFOGRAPHIC]

At the 11th hour, lawmakers in Cyprus, the European Union and the International Monetary Fund have agreed to a €10 billion ($13 billion) bailout of the island country, funded largely by northern European economies (which primarily means Germany).

As part of the deal, Cyprus will have to ante up €5.8 billion of its own. To do that, Cypriot lawmakers have approved an unpopular plan to impose a one-time tax levy on bank depositors' savings. Holders of bank accounts with more than €100,000 will be taxed at 9.9 percent, and those below will have to pay a 6.75 percent levy.

The two sides had until Monday to come up with a bailout plan before euros would have stopped flowing into the country’s banking system; that would have almost certainly sent Cyprus over a fiscal cliff and out of the euro zone, raising questions about the future of the currency bloc. The Cyprus government has about €14 billion in immediate debt to cover, €2.5 billion of which is owned by the Russian government.

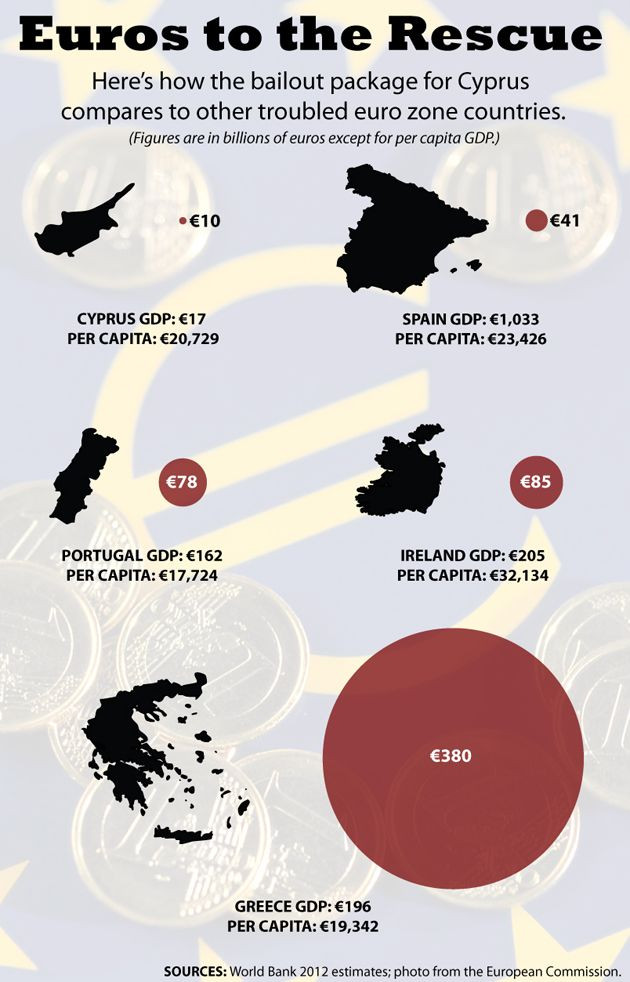

Cyprus is the fifth country in the euro zone to be rescued. Compared to the prior four bailouts -- Spain, Portugal, Ireland and Greece -- the €10 billion price tag is tiny, and relative to the GDP of the four other countries, Cyprus' economy is small as well. However, Cyprus' per capita GDP is above Greece’s and Portugal’s.

Indeed, compared to Spain’s trillion-euro economy, or Greece’s €380 billion bailout (which is much larger than its €196 billion GDP), the money Cyprus needs to stay afloat is a drop in the Mediterranean Sea.

© Copyright IBTimes 2024. All rights reserved.

- MOST POPULAR IN Business