Do I Have To Put Social Security On My Tax Return?

Tax season is about to start, and many taxpayers hope that new tax reform laws will help them pay less in tax this year than in the past. In particular, retirees who rely on Social Security to supplement their savings and provide them with a regular source of income are looking forward to any break they can get from the IRS.

However, one thing that Social Security recipients need to understand as they prepare their returns for the 2018 tax year is that they may have to include some of their benefits as income on their tax returns. Even though the laws governing taxation of Social Security benefits have been on the books for decades, that fact comes as a shock to retirees each and every year, and the structure of the tax seems to snare more and more people every year.

Who has to include Social Security on their tax returns?

The tax laws don't make everyone put their Social Security on their tax returns. Instead, there's an income tax that determines whether you'll end up including a portion of your benefits as taxable income.

The rules governing exactly how much of your Social Security gets taxed involve complex calculations. First, you'll need to come up with your combined income. That includes your adjusted gross income from sources other than Social Security and any nontaxable interest from municipal bonds. It also includes one-half of what you get from Social Security. So if you have $10,000 in income from work and get $24,000 in Social Security benefits, then your combined income will be $10,000 plus half of $24,000. That works out to $22,000.

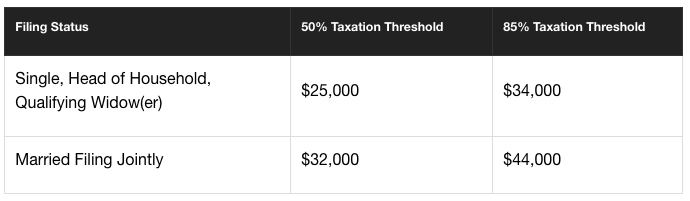

You'll then have to figure out if your combined income is larger than the thresholds for taxing Social Security. The chart below has the key numbers you'll need to know, depending on your filing status.

If your combined income is above the number in the 50% column, then you might have to treat as much as 50% of your Social Security as taxable income. If it's above the number in the 85% column, then the taxable portion rises to as much as 85%.

However, the key words there are "as much as." Often, the amount you have to treat as taxable income is much less than those percentages. For instance, the rules that govern the 50% threshold say that the taxable amount is also limited to 50% of the amount by which your combined income exceeds the threshold. So if you're single and your combined income was $25,100 in 2018, then the most you'll have to include as taxable Social Security benefits is half of the $100 amount by which $25,100 is above the $25,000 threshold. That amounts to just $50 of taxable income, no matter how much Social Security you received.

If you want to run some numbers, the easiest way to do it is by using a calculator. This Social Security income tax calculator lets you consider any scenario you want and then helps you figure out the tax consequences.

Why the problem could get worse

One oddity about Social Security taxation is that the threshold numbers above aren't indexed for inflation. Instead, they've remained basically unchanged since their enactment. Meanwhile, income levels have gradually increased, and as that's happened, more people have to pay taxes on a portion of their Social Security every year.

Unfortunately, since you have limited control over income, it's hard to do much planning to affect the taxation of your Social Security. Just about the only thing you can do is to try to time taxable distributions from retirement accounts in order to keep your combined income under the thresholds, or to put off getting Social Security until your other income won't be as large. Because so many people don't have that level of financial flexibility, more and more taxpayers will find their Social Security benefits subject to tax as time goes by.

This article originally appeared in the Motley Fool.

The Motley Fool has a disclosure policy.

- MOST POPULAR IN Business