Dollar Continues Dream Run, Little Stands In Its Way

The U.S. dollar will remain strong for at least the next three months as it basks in both expectations for aggressive Federal Reserve interest rate rises and safe-haven appeal stemming from global recession fears, a Reuters poll of FX analysts showed.

The recent sell-off in risk assets and bond markets is also playing into a broad dollar rally against nearly every other currency, to levels not seen in two decades. Analysts say there is no good reason to expect it to stall yet.

Already up a hefty 7% last year, the dollar has soared another 12% this year, consistently exceeding nearly every forecaster's expectations on how long its winning streak would last.

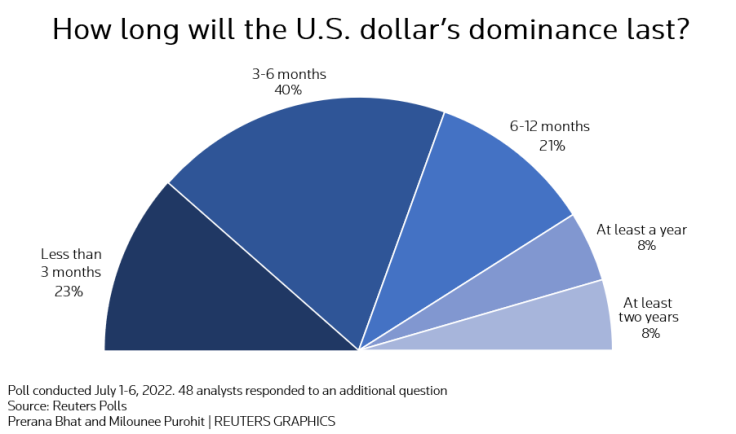

A three-quarters majority of analysts, 37 of 48, in a separate question from the July 1-6 Reuters FX poll expect that trend to continue for at least another three months.

Of those, 19 said three to six months, 10 said six to 12 months, four said at least a year and four said at least two years. Only 11 respondents said less than three months.

Yet despite near-term strength, the median forecast from the latest poll of nearly 70 analysts doggedly clings to a long-held view that the dollar will weaken in the coming 12 months, despite the euro now trading at its weakest in two decades.

Graphic: Reuters Poll- Foreign exchange poll-July 2022,

"Ultimately, people who say the dollar is going to weaken because the market is not pricing in as many interest rate hikes from the Fed as before are forgetting that the dollar is also a safe haven," said Jane Foley, head of FX strategy at Rabobank.

"If we are, coincidentally, looking at a potential recession in the euro zone and the UK, and if global growth is coming down...what are you going to buy if you sell the dollar?"

While the lack of alternatives is likely to keep the dollar well-bid against nearly all currencies, the greenback's strength will be most acutely felt by the ones who have little to no interest rate backing them.

Indeed, the euro, the Japanese yen and the British pound, whose central banks have either not hiked rates or failed to keep up with the Fed's aggressive policy tightening, have weakened by double-digit percentages this year.

Minutes of June's policy meeting revealed concerns that worsening inflation would erase faith in the Fed's ability to control it. That has pushed the central bank to embark on the most aggressive tightening cycle in decades - knocking markets on recession fears.

Down over 10% for the year, the euro is forecast to gain nearly 8.0% to around $1.10 by mid-2023, according to the median.

However, that 12-month view was the lowest median 12-month euro prediction in five years, and nine analysts expect it to reach or breach parity by mid-2023.

The Japanese yen, the worst performer among majors, is down nearly 15% for the year and will likely remain weaker than 130 per dollar over the next six months on the gap between Japanese and U.S. benchmark yields and monetary policy. [JPY/POLL]

Sterling, down nearly 12% against the dollar since the start of this year, is expected to regain around half of its lost ground in 2022 over the next year as the Bank of England looks set to continue raising interest rates. [GBP/POLL]

But in the near-term, a host of issues is likely to keep the currency under pressure.

Emerging market currencies will also struggle to stem losses against the greenback in the near-term as investors seek the safety of dollar denominated assets.

While China's tightly controlled yuan, the Indian rupee and the Malaysian ringgit were predicted to trade around where they are now over the next three to six months, the Russian rouble and Turkey's lira were expected to fall.

(For other stories from the July Reuters foreign exchange poll:)

© Copyright Thomson Reuters 2024. All rights reserved.

- MOST POPULAR IN Economy & Markets