A Fed Soft Landing For Jobs Means Something Else Has To Crack; So Far It Hasn't

The healthy finances of U.S. banks, companies and households, trumpeted during the pandemic by Federal Reserve officials as a source of resilience, may be an obstacle to battling inflation as central bankers raise interest rates in an economy able so far to pay the price.

In outlining their aggressive turn to tighter monetary policy, Fed officials say they hope to clamp down on the economy without destroying jobs, with higher interest rates slowing things enough that companies scale back the current high number of job vacancies while avoiding layoffs or a hit to household income.

But that means the pain of inflation control would have to fall mostly on owners of capital via a slowed housing market, higher corporate bond rates, lower equity values, and a rising dollar to make imports cheaper and induce domestic producers to hold down prices.

Economists including current and former Fed officials note that unlike prior Fed rate hike cycles, there's no obvious weakness to exploit or asset bubble to burst to quickly make a dent in inflation - nothing akin to the highly overvalued housing markets of 2007 or the hypervalued internet stocks of the late 1990s to provide the Fed more bang for its expected rate hikes.

The adjustment to tighter Fed policy has been swift by some measures. But it has been spread moderately across a range of markets, none catastrophically, with little impact yet on inflation or consumer spending.

That may come. Piper Sandler economists Roberto Perli and Benson Durham recently estimated that financial conditions have tightened faster than in any Fed cycle since at least the early 1990s, and should slow economic growth "to about 1% by the end of the year," about half the economy's underlying trend.

But the waiting game could itself mean a harder struggle for the Fed.

The depth of the problem depends on how fast and how close the Fed wants inflation to get back to its 2% target from roughly triple that now, said Donald Kohn, a former Fed vice chair now at the Brookings Institution.

"The question is how far does inflation come down in the easy part of the cycle" when growth may slow and unemployment rise by a small amount, but before interest rates have gotten so high the economy falters, Kohn said. "I am skeptical that's enough to get inflation back to the two range. To get the last percentage point...they are going to have to tighten more, and whether they can do that without a recession is an open question."

GOOD NEWS, BAD NEWS

So far the pieces are not obviously fitting together.

The Fed has raised its short-term interest rate by three-quarters of a percentage point this year and intends to keep at it with half-point increases at its meeting next week and again in July. More will likely follow.

While credit markets have responded with sharp increases in home mortgage rates, for example, and equity markets with falling stock prices, there's little evidence that has translated yet into substantially lower demand or a substantial decline in inflation.

Home prices are still rising, though the pace may slow as sales ebb. The S&P 500 has dropped 13% this year, and the decline in equity values should, economists argue, feed into lower consumer spending. But the index is also now roughly where it would have been had pre-pandemic growth rates continued - hardly a collapse.

Corporate credit spreads have risen, potentially stressing weaker borrowers or leading to pared expansion or investment spending. But the Fed's most recent financial stability report noted debt service costs remained low. A New York Fed corporate bond distress index has risen this year, but peaked as Russia invaded Ukraine in February and has fallen through the Fed's first rate hikes.

Consumer spending remains strong, companies continue adding hundreds of thousands of workers a month at higher wages, and some metrics the Fed is watching, like job vacancy rates, have yet to subside.

The good news: That keeps the hoped-for narrative of inflation control without job loss in play.

The bad news: Beyond some moderation in month-to-month inflation numbers, there's little sense the pace of price increases has broken.

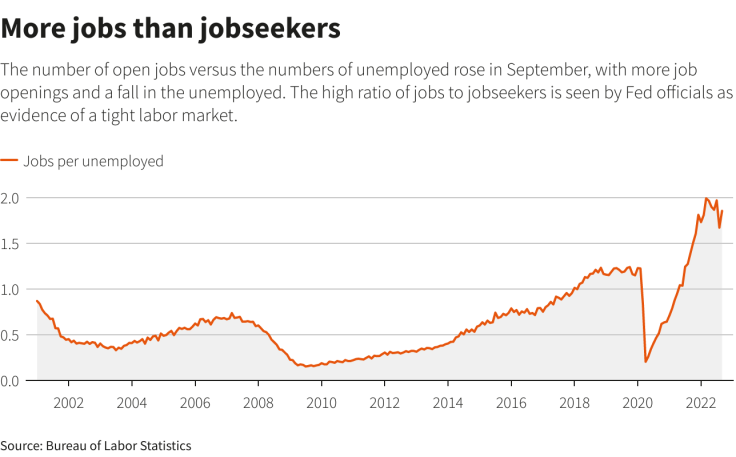

Graphic: Unemployed to job openings -

THE 'WILD CARD'

Policymakers next week will provide fresh economic and interest rate projections. The latest consumer inflation data will be released Friday and is expected to show prices still rising by more than 8% annually, a pace not seen since the 1980s.

Deutsche Bank Chief Economist Matthew Luzzetti estimated Fed progress on inflation will require financial conditions to tighten further - perhaps enough to cause another 10% selloff in stocks, or a full 100-basis point rise in the spread between investment grade corporate bond yields and Treasuries.

That would "help to tame inflation pressures while at least theoretically keeping open a path to a soft landing," Luzzetti wrote.

The Fed is, in a sense, racing against the clock. The more it struggles to curb demand and the longer inflation persists, the more policymakers may worry that higher inflation is becoming embedded and in need of a more aggressive response.

A big unknown is how much help will come through other channels such as improvement in the movement of goods out of China or of food and other commodities out of Ukraine.

The flow of workers into jobs could also help. As more people join the labor force, relocate for work, or retrain, vacancies may fall not, as they often do, because the economy is weakening, but because of more efficient hiring.

Like changes in productivity, those are ways the Fed may get help on inflation without higher borrowing costs, the central bank equivalent of a free lunch.

In a recent interview, Citi Chief Global Economist Nathan Sheets said Fed policy will still work through its standard channels, with a slowed housing market, for example, lowering demand for purchases of furniture and appliances.

But given the size of the inflation shock, and the uncertainty over how much help will come from elsewhere, the adjustment may have to be that much tougher.

"If we don't get that improvement in those supply shocks...that means these measures of financial conditions we're looking at are going to need to tighten potentially significantly," Sheets said. "What makes me not entirely confident is the whole issue of how much slowing...how much rise in unemployment, how much reduction in the output gap is going to be necessary...to bring inflation down. That's the wild card."

© Copyright Thomson Reuters 2024. All rights reserved.

- MOST POPULAR IN National