Markets To Central Bankers: We Don't Believe You

Central bank policy announcements, once viewed as the rule book for how markets should move, are not resonating with traders any more.

Take Wednesday's Federal Reserve rate move. The central bank lifted its main funds rate by 25 bps to its highest since 2007 as it continued its fight against inflation.

Yet the S&P 500 hit a five-month high, as traders focused resolutely on the idea that the world's most influential central bank would change course soon.

Government bond markets meanwhile continued to price in rate cuts by year-end as the economic cycle turns.

Over in Europe, the European Central Bank delivered a hefty 50 bps hike on Thursday and promised more of the same for March and beyond.

Euro zone markets also rallied. The Stoxx 600 share index hit its highest since April, Germany's 10-year bond yield slid 23 bps, its largest fall in almost a year, as its price surged. Italian yields posted their biggest one-day fall since the ECB unleashed emergency stimulus during the 2020 COVID-19 crisis.

"Markets are saying 'you can say what you want right now, we know you'll change your tune,'" said Salman Ahmed, global head of macro and strategic asset allocation at Fidelity International.

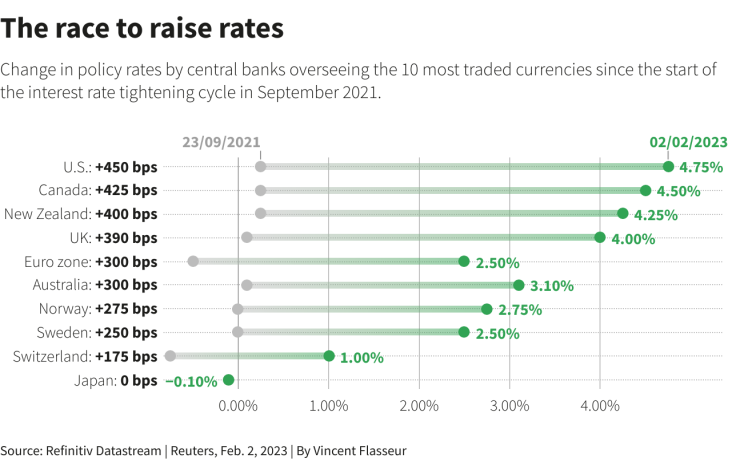

GRAPHIC: The race to raise rates The race to raise rates -

DISCONNECT

Investors said that whatever central banks pledged now mattered less for markets already driven by a belief that inflation has peaked. Markets also anticipate the lagged effect of rate rises would slow the global economy, with both forcing rate hikes to be reversed later in the year.

Traders expect the Fed to cut rates at least twice by year-end. Even as the ECB sounded hawkish, markets lowered expectations for where its key rate will end up to around 3.25% from 3.4% earlier on Thursday.

Fed chair Jerome Powell said on Wednesday that "I just don't see us cutting rates this year." ECB president Christine Lagarde said "we have more ground to cover and we are not done."

"What you're seeing here is the market saying okay, the Fed is going to hike, but ultimately, it's going to need to come back down at some point," said Jeffrey Sherman, Deputy CIO at DoubleLine Capital, which manages almost $100 billion in assets, referring to inflation easing.

U.S. headline inflation has dropped from a 40-year high last year to 6.5%. In the euro zone, hit by an energy crisis related to Russia's war in Ukraine, headline inflation at least moderated to 8.5% last month.

Ten-year Treasury yields are down 50 bps so far this year to around 3.3%, having soared 236 bps last year.

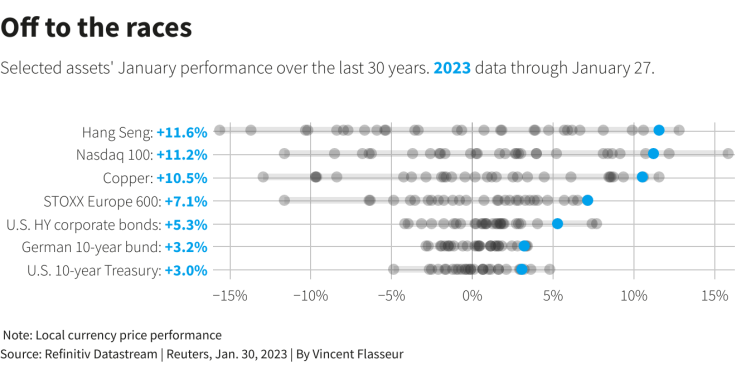

GRAPHIC: Off to a great start -

GOOD REASON

Central bankers have good reason to talk tough. Exuberant markets risk undermining their tightening efforts.

"They have continued to sound quite hawkish but the market doesn't really believe them," said Sebastian Mackay, multi-asset fund manager at Invesco.

"In terms of the impact of (central bank) hawkishness on markets," he added, "this has significantly softened."

Markets also price a scenario where major economies cool down just enough to prompt central banks to quit hiking rates, without plunging into dreadful recessions.

Meanwhile price action following this week's central bank meetings continued a months-long cross-asset rally.

The S&P 500 and Europe's Stoxx index have rallied over 8% each since the start of this year. A Bank of America index of U.S. Treasury bonds has risen about 3%.

UK gilt yields meanwhile also tumbled after the Bank of England on Thursday signalled the tide was turning in its battle against high inflation after it raised rates again.

Risky assets are not usually expected to rise with government bonds, which investors use to shelter their portfolios against economic downturns. Still, markets were somehow managing to price "the best of all worlds," said Joseph Little, chief global strategist at HSBC's asset management unit.

Government bonds, whose coupon payments are eroded in real terms by inflation, were rallying in expectation of energy price shocks and supply chain issues caused by COVID shutdowns "becoming more benign," Little said. Equities and corporate bonds, he added, were predicting that easing inflation would "feed in to corporate profits".

Some investors believed markets are also underestimating the full impact of monetary tightening that operates with a time lag.

"This tightening was not done on planet Mars. This was done on planet Earth and somebody has to pay for this tightening," said Fidelity's Ahmed.

© Copyright Thomson Reuters 2024. All rights reserved.

-

Nature Pays Price For War In Israel's North

-

Cracks Deepen In Canada's Pro-immigration 'Consensus'

-

Mexico City Youth Grapple With Growing Housing Crisis

-

Greece's Ambitious 'Smart City' By The Sea Takes Shape

-

Dating Apps Move To Friend Zone In Search Of Profits

-

In Colombia, A River's 'Rights' Swept Away By Mining And Conflict

-

How China's Censorship Machine Worked To Block News Of Deadly Attack

-

Surfboards With Bright Lights Could Deter Shark Attacks - Researchers

-

Nations To Submit Boosted Climate Plans: What's At Stake?

-

Bees Help Tackle Elephant-human Conflict In Kenya