Nearly Four Years After China Eased Its Currency Policy, Yuan-Held Deposits In Hong Kong Have Ballooned More Than 500%

China has long had the ambition of seeing its currency, the yuan, challenge the hegemony of the U.S. dollar. If recent history is any indication, the country is well on its way to achieving that goal.

One of main reasons for its progress toward that goal has been Beijing's willingness to gradually surrender at least some control of the yuan's value to the world market.

For years China undervalued the yuan to make its exports more competitive. It worked, but at the price of provoking major trading partners, like the U.S. and Europe. The issue emerged as a point of contention during the last U.S. presidential race, with Republican candidate Mitt Romney lambasting President Barack Obama for not doing enough to get China to begin valuing its currency more fairly.

China has been more than aware of such criticisms, and it has been responding, albeit slowly. In 2009 it began a pilot program of internationalizing its currency by allowing Hong Kong banks to trade the yuan.

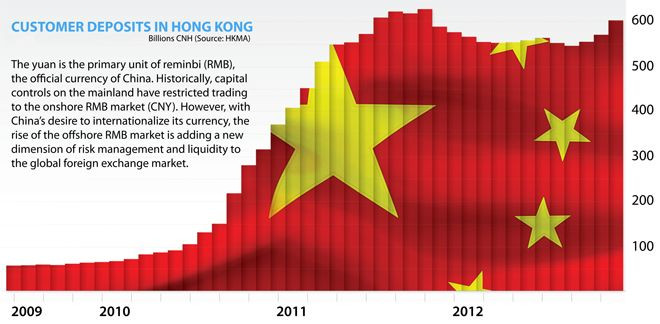

And since then the number of yuan-held deposits in Hong Kong has exploded, from less than 100 billion in the first half of 2010 to about 600 billion in 2013. Also in 2010, China eased the yuan back to a managed float after it established a completely fixed currency in 2008 as an emergency response to the American subprime mortgage meltdown.

In January 2011, the Chinese began allowing Americans to trade in the currency; and China-based companies were allowed for the first time to use the yuan for business outside the mainland. By October 2011, foreign companies were allowed to settle direct investments on the mainland using the yuan.

Then last year, Beijing eased the yuan’s trading band against the dollar for the first time in five years – allowing the currency to fluctuate more broadly.

This rapid growth in off-the-mainland yuan deposits caught the attention of the Chicago Mercatile Exchange, which announced Monday it would join Hong Kong Exchanges and Clearing Limited (HKG:0388) and start trading CNH futures under contracts of up to three years.

Letting the yuan float freely with the ebb and flow of the global currency market could give a boost to economies that depend on exports to China. The downside, however, to that is the initial shock to the economy that can occur when a currency that is artificially under- or overvalued suddenly sees an overnight adjustment, as occurred when Mexico allowed its peso to float freely at the end of 1994. (It took a decade for the country to begin benefiting from the move, according to The Financial Times.)

But China isn’t Mexico. In addition to the concerns over a deep economic blow that could destabilize the country, a Chinese economic crisis like the one in the mid-'90s that hit Mexico – which was the first developing country to let its currency float freely – would have global repercussions.

© Copyright IBTimes 2024. All rights reserved.

- MOST POPULAR IN Business