Peak Interest Rates May Be Lower Than Expected As Growth Slowdown Looms

Worsening economic data may force central banks to blink and take a less aggressive rate-rise stance, money markets are betting, having steadily dialled back expectations of where U.S. and British interest rates might peak.

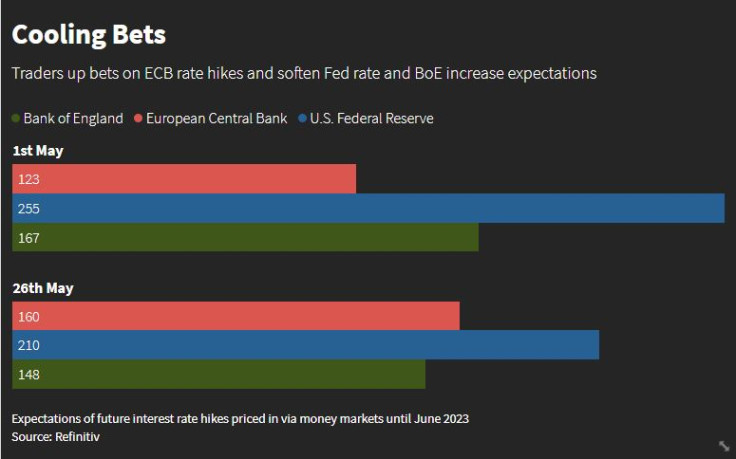

The equivalent of a half-point rate hike from the Federal Reserve has been priced out over the last three weeks, putting the peak in rates at 3% next June.

That implies cumulative U.S. rate hikes of 210 basis points this cycle, versus 255 bps at the start of May, according to Fed Fund futures that reflect expectations of future interest rate moves.

In Britain too, despite expectations of 10% inflation this year, recession signals are forcing a shift, with 120 bps of rate rises priced until June 2023, from 165 bps at the start of May. That would take rates to around 2.4%.

Graphic: RATE BETS -

"What the market is doing now is focusing less on inflation and more on the risk of recession, that's why we are seeing this repricing," said Flavio Carpenzano, investment director at Capital Group.

"Markets also believe in the so-called Fed put, that when we get tighter financial conditions and equity markets fall 20% the Fed will step in."

He was referring to the long-held belief that the U.S. central bank will backstop falling stock markets by going easy on rate-tightening.

Global stocks have indeed perked up this week as money markets repriced, snapping a seven-week falling streak. But Carpenzano does not believe the Fed can ease its stance, given inflation is running at four times the target rate.

"If you have inflation running higher than 0.5% month to month, the Fed will have to go quite hawkish," he said.

Correctly forecasting a Fed pivot is the holy grail for financial markets, given world stocks have shed trillions of dollars in value since the United States and other developed economies kicked off policy tightening.

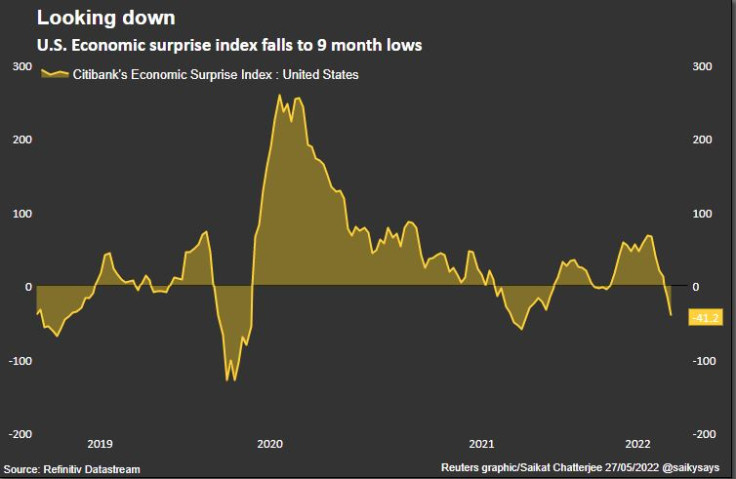

The money market pullback may be unsurprising, given slowing U.S. housing markets and a series of weak data that pushed Citi's Economic Surprise Index to one of its steepest four-week declines in the past 20 years.

Also potentially signalling some room to manoeuvre, the key Personal Consumption Expenditures (PCE) price index gained just 0.2% last month after shooting up 0.9% in March, suggesting inflation may have peaked.

Graphic: CESI USD -

Goldman Sachs now sees a 35% probability of a U.S. recession during the next two years but expects dividends to fall in any case -- an event that has never happened outside of a recession. Some Fed officials such as Raphael Bostic have urged caution on policy tightening.

Laura Cooper, a senior investment strategist at Blackrock, predicts "a dovish tilt" from the Fed by year-end, as "policymakers become more data-dependent beyond the two 50 bps rate hikes priced in by the market over the next two meetings."

Thomas Costerg, senior economist at Pictet Wealth, expects the Fed to pause after two 50 bps rate hikes, noting U.S. financial conditions are already at the tightest in two years.

"You could actually argue that 75% of the job has been done already," Costerg said, adding that sub-2% U.S. GDP growth -- which he expects by year-end -- is usually disinflationary.

In Britain, where recession is more likely, the Bank of England may find it harder to back off.

A ?15 billion government spending package announced this week means "the BoE will need to hike into contractionary territory," Goldman wrote, predicting 25 bps back-to-back rate rises through February 2023, taking the terminal rate to 2.5%.

Finally, for the European Central Bank, tightening bets have ramped up, with 160 bps of rate hikes expected in the coming year, from 123 bps in early-May. ECB boss Christine Lagarde has signalled rates, currently at -0.5%, will be at 0% or above by September.

"The ECB will use this as an opportunity to get rid of negative interest rates and any Fed pivot is unlikely to change that," Pictet's Costerg added.

© Copyright Thomson Reuters 2024. All rights reserved.

- MOST POPULAR IN Economy & Markets