Record High U.S. House Prices, Rising Mortgages Depress New Home Sales

Sales of new U.S. single-family homes tumbled to a two-year low in April, likely as higher mortgage rates and record prices squeezed first-time buyers and those in search of entry-level properties out of the housing market.

The fourth straight monthly decline in sales reported by the Commerce Department on Tuesday added to data last week showing a plunge in single-family building permits in April and continued weakness in sales of previously owned homes in suggesting that demand for housing was cooling.

But the housing market slowdown is likely to be limited by record low inventory. It is the segment of the economy most sensitive to interest rates. The Federal Reserve is raising borrowing costs to dampen domestic demand and tame inflation.

"Activity in the housing market has cooled significantly in recent months along with the recent jump in mortgage rates," said Daniel Silver, an economist at JPMorgan in New York. "While higher rates likely have been weighing on sales, limits in available inventory and high house prices also may be restraining activity."

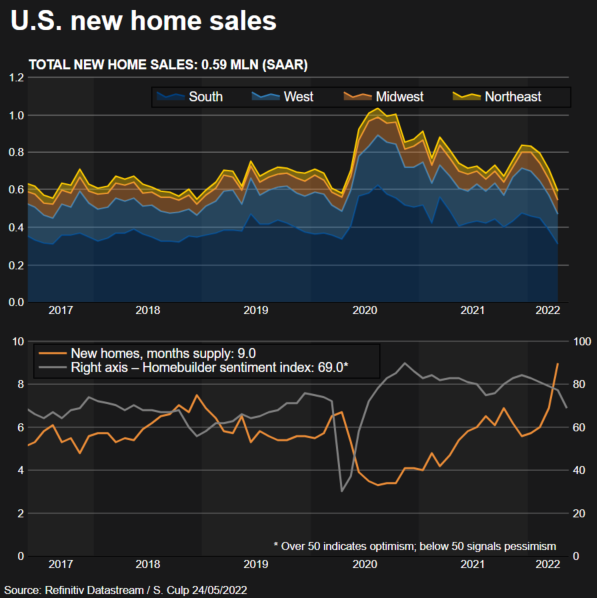

New home sales plunged 16.6% to a seasonally adjusted annual rate of 591,000 units last month, the lowest level since April 2020. March's sales pace was revised down to 709,000 units from the previously reported 763,000 units. Sales dropped 5.9% in the Northeast and tumbled 15.1% in the Midwest. They plummeted 19.8% in the densely populated South and decreased 13.8% in the West.

Economists polled by Reuters had forecast that new home sales, which account for 9.5% of U.S. home sales, would fall to a rate of 750,000 units. Sales dropped 26.9% on a year-on-year basis in April. They peaked at a rate of 993,000 units in January 2021, which was the highest level since the end of 2006.

Graphic: New home sales -

Though volatile on a month-on-month basis, new home sales are a leading indicator for the housing market as they are counted at the signing of a contract.

Stocks on Wall Street were lower. The dollar slipped against a basket of currencies. U.S. Treasury prices rose.

REDUCED AFFORDABILITY

The 30-year fixed-rate mortgage jumped above 5% in April for the first time since February 2011, according to data from mortgage finance agency Freddie Mac. It has surged, averaging 5.25% in the week ending May 19.

The Fed has hiked its policy interest rate by 75 basis points since March. The U.S. central bank is expected to raise that rate by half a percentage point at each of its next policy meetings in June and July.

Data last week showed sales of previously owned homes dropped to a two-year low in April, while single-family building permits were the lowest since last October. Single-family homebuilder confidence was near a two-year low in May.

Though the softening housing market could weigh on economic growth this quarter, economists were not ringing alarm bells.

"The housing market is now back to pre-pandemic levels, so this massive hit in April should not be construed as the popping of a bubble," said Jeffrey Roach, chief economist at LPL Financial in Charlotte, North Carolina.

The moderation in sales gains could allow supply to increase and slow double-digit price growth. The median new house price in April soared 19.6% from a year ago to a record $450,600. The average house price surged at a much faster 31.2% to $570,300, which suggested stronger price gains on lower-end homes.

"Combine that with a significant increase in financing costs and increased price sensitivity in the starter home market and it appears builders passing through costs was a significant factor in the sales drop, perhaps as significant as the mortgage rate increase," said Chris Low, chief economist at FHN Financial in New York.

Virtually all the houses sold last month were above the $200,000 price level. There were 444,000 new homes on the market at the end of April, up from 410,000 units in March. Houses under construction made up roughly 65% of the inventory, with homes yet to be built accounting for about 27%.

The backlog of homes approved for construction but yet to be started is at an all-time high as builders struggle with shortages and higher prices for inputs like lumber for framing, as well as cabinets, garage doors, countertops and appliances.

At April's sales pace it would take 9.0 months to clear the supply of houses on the market, up from 6.9 months in March.

Slowing activity was also evident in a survey from S&P Global on Tuesday showing its flash U.S. Composite PMI Output Index, which tracks the manufacturing and services sectors, fell to a reading of 53.8 in May from 56.0 in April.

The slowest growth pace in four months was attributed to "elevated inflationary pressures, a further deterioration in supplier delivery times and weaker demand growth." A reading above 50 indicates expansion in the private sector.

"It is likely still too soon to tell if recent declines simply reflect a return to pre-pandemic patterns or a possibly deeper slowing," said Veronica Clark, an economist at Citigroup in New York.

© Copyright Thomson Reuters 2024. All rights reserved.

- MOST POPULAR IN National