S&P 500, Dow Close Lower After Bank Earnings, Inflation Data

The S&P 500 pared early losses to close modestly lower on Thursday after investors digested disappointing quarterly results from two large U.S. banks and hotter-than-expected inflation data.

Initially, all three major U.S. stock indexes sold off sharply in the wake of second-quarter earnings from JPMorgan Chase & Co and Morgan Stanley. Both reported slumping profits and warned of impending economic slowdown.

Losses narrowed as the session wore on, with advancing microchip stocks helping nudge the Nasdaq Composite Index to a nominal gain.

"There was an irrational response to the JPMorgan and Morgan Stanley results," said Jay Hatfield, chief executive and portfolio manager at InfraCap in New York. "It wasn't a surprise that investment banking was weak."

"JPMorgan warned that there's uncertainty in the market, but if you're alive and breathing you know there's uncertainty in the market."

JPMorgan CEO Jamie Dimon struck a cautious note on the global economy while Morgan Stanley's investment banking unit struggled to cope with a slump in global dealmaking.

Shares of JPMorgan Chase and Morgan Stanley fell 3.5% and 0.4%, respectively, while the S&P Banks index shed 2.4%.

Slowdown worries were exacerbated as the Labor Department's Producer Price Index report echoed Wednesday's Consumer Price Index data, showing hotter-than-expected inflation in June.

The sell-off began to ease after Fed Governor Christopher Waller said he supported another 75 basis point interest rate increase in July, easing jitters over an even bigger, 100 basis point hike.

"The Fed is going to rise rates by 75 but they shouldn't," Hatfield said. "The Fed has already done a lot to reduce inflation but they're not going to realize that until they see it in the rear view mirror."

"The thing to remember about the Fed is it's almost as if their third mandate is to be behind the curve," Hatfield added.

On Wednesday, the odds of a larger hike grew after the CPI report, considering the central bank's intention to aggressively tackle decades-high inflation - a prospect which increases chances of an economic contraction.

"There will be a recession but a mild one," said Oliver Pursche, senior vice president at Wealthspire Advisors, in New York. "The key component is continued strength in the labor market. Given where we are in the employment picture, that's not an immediate threat."

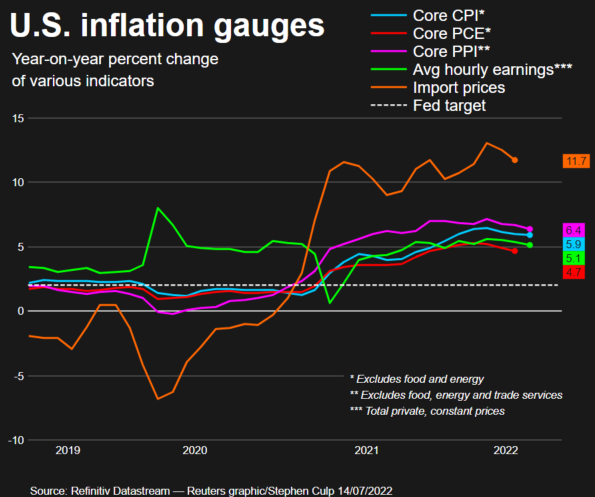

Core inflation, which strips out food and energy prices, continues to ease from the March peak, although it remains well above the central bank's average annual 2% target:

(Graphic: Inflation:

)

The Dow Jones Industrial Average fell 142.62 points, or 0.46%, to 30,630.17, the S&P 500 lost 11.4 points, or 0.30%, at 3,790.38 and the Nasdaq Composite added 3.60 points, or 0.03%, at 11,251.19.

Eight of the 11 major sectors of the S&P 500 ended the day in negative territory, with financials suffering the largest percentage loss, dropping 1.9%.

Tech was the biggest gainer.

With earnings season officially underway, analysts expect aggregate S&P 500 second-quarter year-on-year profit growth of 5.1%, far less than the 6.8% estimate at the beginning of the quarter, according to Refinitiv.

U.S.-listed shares of Taiwan Semiconductor Manufacturing rose 2.9% following the chipmaker's upbeat revenue guidance.

Conagra Brands tumbled 7.2% after issuing an annual earnings forecast that came in below estimates.

Declining issues outnumbered advancers on the NYSE by a 3.11-to-1 ratio; on Nasdaq, a 2.12-to-1 ratio favored decliners.

The S&P 500 posted one new 52-week high and 44 new lows; the Nasdaq Composite recorded nine new highs and 294 new lows.

Volume on U.S. exchanges was 10.86 billion shares, compared with the 12.48 billion average over the last 20 trading days.

© Copyright Thomson Reuters 2024. All rights reserved.

- MOST POPULAR IN Economy & Markets