Stocks Suffer Renewed Slide On Growth Fears, Dollar Extends Rally

Stocks fell heavily again on Monday and the dollar rocketed to a new two-decade high as worries about higher interest rates and a tightened lockdown in Shanghai deepened investors' fears that the global economy is rapidly heading for a slowdown.

After a bruising session on Friday in which U.S. stocks sold off sharply as another rise in long-dated U.S. Treasury yields unnerved investors, markets were set for a rocky start to the week, with most indexes in the red.

Central banks in the United States, Britain and Australia all raised interest rates last week, and investors are bracing for more tightening as policymakers try to get on top of soaring inflation.

"We see recession risk over the next 12 to 18 months to be as high as about 30%," said Dan Ivascyn, group chief investment officer at bond giant PIMCO.

"One of the key reasons for that is the Fed and other central banks appear dead set on getting inflation under control."

There was plenty more for investors to worry about on Monday aside from tightening financial conditions.

There appeared to be no let-up in China's zero-COVID policy, with Shanghai tightening the city-wide lockdown for 25 million residents.

Speculation that Russian President Vladimir Putin might declare war on Ukraine in order to call up reserves during his speech at "Victory Day" celebrations also hurt market sentiment. Putin has so far characterised Russia's actions in Ukraine as a "special military operation", not a war.

Wall Street futures headed sharply lower with the S&P 500 futures down 2% and Nasdaq futures 2.5%. The S&P 500 and Nasdaq on Friday posted their fifth straight week of declines -- their longest losing streak in a decade.

The Euro STOXX weakened 2%. Germany's DAX lost 1.6% and Britain's FTSE 100 1.78%.

MSCI's main emerging market stocks index fell 1.2% to its lowest level since July 2020.

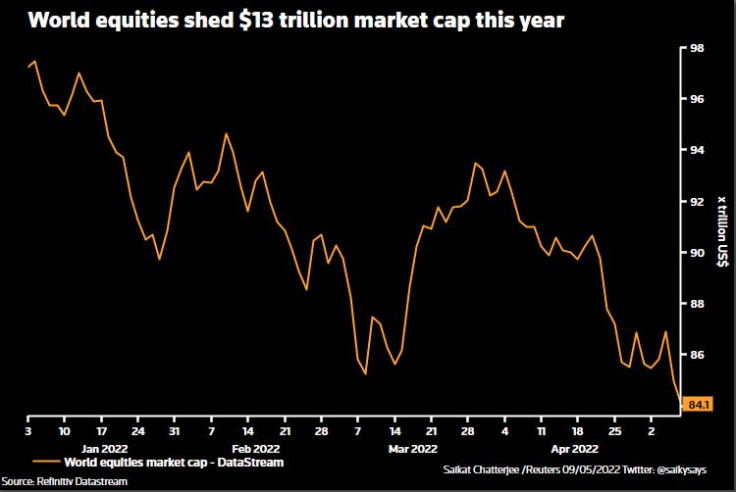

The MSCI World Index dropped 0.7%, leaving it not far from the 17-month intraday low reached on Friday.

(Graphic- World equities:

)

MSCI's broadest index of Asia-Pacific shares outside Japan fell 1.4% and Japan's Nikkei 2.53%. Chinese blue chips eased 0.8%, while in offshore markets the yuan fell to as low as 6.7759 per dollar, its weakest since October 2020.

The big data event of the week is the U.S. consumer price report due on Wednesday, when only a slight easing in inflation is forecast, and certainly nothing to prevent the Federal Reserve from hiking by at least 50 basis points in June.

U.S. 10-year bond yields on Monday reached a new 3-1/2 year high of 3.203%.

DOLLAR DOMINANCE

With investors juggling so many worries, one place they are looking for safety is in the dollar.

The dollar index, which measures the greenback against a basket of currencies, rose as much as 0.4% to 104.19, the latest in a string of 20-year highs.

"Risk appetite is fragile and yield spreads continue to suggest further upside on the Dollar Index," said Sean Callow, a senior FX strategist at Westpac.

"We look for ongoing demand for DXY (the dollar index) on dips, with 104 already being probed and still potential for a run towards 107 multi-week."

The soaring dollar is hammering other currencies. The euro briefly dropped back below $1.05 while the Japanese yen fell to its weakest since 2002.

Expectations that the Fed will move more aggressively in raising interest rates are supporting the dollar, as is a sense among investors that the U.S. economy will hold up better than a euro zone hit by the fallout from the war in Ukraine.

But rates are also rising in the euro zone. On Monday, Germany's 10-year bond yield hit a new highest level since 2014, buoyed by hawkish policymaker Robert Holzmann saying on Saturday that the European Central Bank should raise rates three times this year to combat inflation.

The diary is full of Fed speakers this week, giving them plenty of opportunity to keep up the hawkish chorus.

Oil prices initially see-sawed after the Group of Seven nations committed to banning or phasing out imports of Russian oil over time, before falling.

Brent dropped 2.15% at $109.97 by 1115 GMT, while U.S. crude dropped 2.39% to $107.15. [O/R]

Spot gold prices lost 1.24% to $1,859 an ounce, having struggled recently to gain traction as a safe haven. [GOL/]

© Copyright Thomson Reuters 2024. All rights reserved.

- MOST POPULAR IN Economy & Markets