One Industry Amazon Is Set To Disrupt

Amazon (NASDAQ:AMZN) has expanded its retail business from books to almost everything under the sun, but one area it's been slow to enter is food. The company made a big move into food retail by acquiring Whole Foods, but its grocery delivery business is small and has focused primarily on non-perishable items so far.

I don't know if Amazon is going to get into the home food delivery business, but I think it's the perfect company to disrupt commercial distributors like Sysco Corporation (NYSE:SYY), US Foods Holding Corp (NYSE:USFD), and Performance Food Group (NYSE:PFGC). At their core, these companies distribute products -- and no company is more nimble than Amazon at distributing products. That should scare the stagnant food distribution competitors.

Amazon is eyeing foodservice

Slowly but surely Amazon is creeping its way into the foodservice industry. Brands from General Mills (NYSE:GIS)to Kraft (NASDAQ:KHC) to McCormick (NYSE:MKC) have built brand pages on Amazon and started selling products through its online platform. They aren't abandoning traditional distribution channels right now, but they're exploring the possibility of selling directly to customers.

In food service, going directly to restaurants and other food preparers would be a good financial move. It would eliminate a layer of distribution and allow companies to leverage their own sales staffs, rather than layering sales staff on top of distribution sales staff.

From an operational standpoint, Amazon could add a lot of value to customers in food service. The company can deliver more quickly than distributors with smaller volumes on shorter notice. In a business where shelf space is critical and inventory can't sit for long, those are keys to more efficient operations.

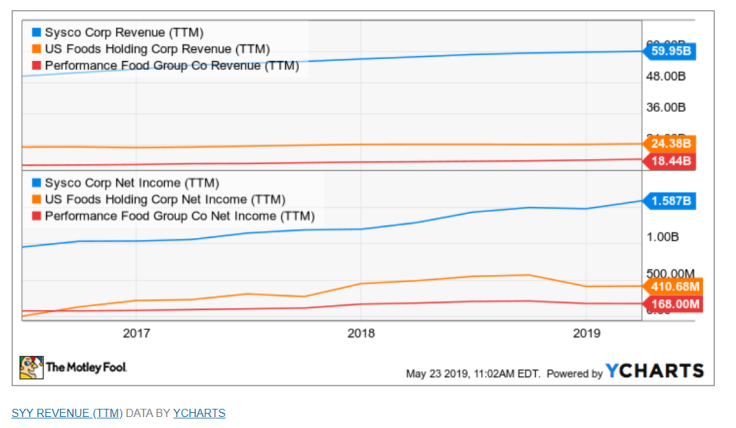

There aren't signs of trouble... yet

Revenue at the biggest food service distributors has been growing slowly over the last few years, and net income is rising (partly due to tax cuts). At Sysco, organic growth in food service was 2.7% in the first three quarters of fiscal 2019 and net income is ticking higher, which seems healthy right now.

What shouldn't be lost is that consolidation is helping keep growth and margins intact. In the last year, Sysco has acquired Kent Frozen Foods, Doerle Food Service, J&M Wholesale Meats, and Imperio Foods to expand its presence. As it consolidates it gains pricing power, which helps the bottom line and even allows it to raise prices. But that may not last forever.

A new way to shop

It'll take time for food brands to move their business to an online store like Amazon. They've been distributing through traditional channels for so long that it's a difficult ship to turn around. But new restaurants are used to shopping online, and are already using Amazon for everything from napkins to cleaning wipes. Why not add some pizza sauce or vegetables to that order?

When more food products are available online, Amazon could become a go-to supplier for food service customers. That should scare distributors, who may need to adapt their business models in ways that are out of their core competency. And that's where Amazon thrives: in its disruption of existing businesses.

John Mackey, CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool's board of directors. Travis Hoium has no position in any of the stocks mentioned. The Motley Fool owns shares of and recommends Amazon. The Motley Fool recommends McCormick. The Motley Fool has a disclosure policy.

This article originally appeared in The Motley Fool.

- MOST POPULAR IN Business