Is The U.S. In A Recession? Jobs And GDP Tell A Different Story

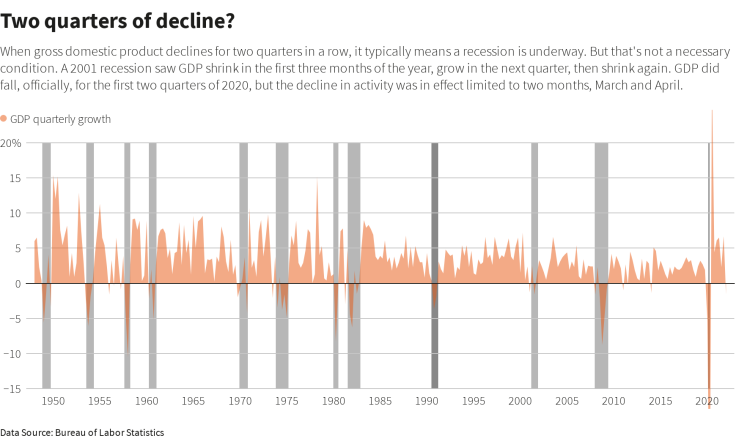

By some early estimates, the U.S. economy, as measured by gross domestic product, may have shrunk in the three months from April through June. Add that to the decline from January through March, and that would be a contraction for two quarters in a row.

By an often-cited rule of thumb, that means the world's largest economy is in recession.

But deciding when a recession has begun or predicting when one might occur is not straightforward.

The "two quarters" definition is handy for analysts, journalists and the general public. But it is not how economists think about business cycles, partly because GDP is a broad measure that can be influenced by factors like government spending or international trade.

Instead they focus on data on jobs, industrial production, spending and incomes - and job growth in particular remains strong in the United States, with U.S. employers hiring more than expected in June, and raising wages.

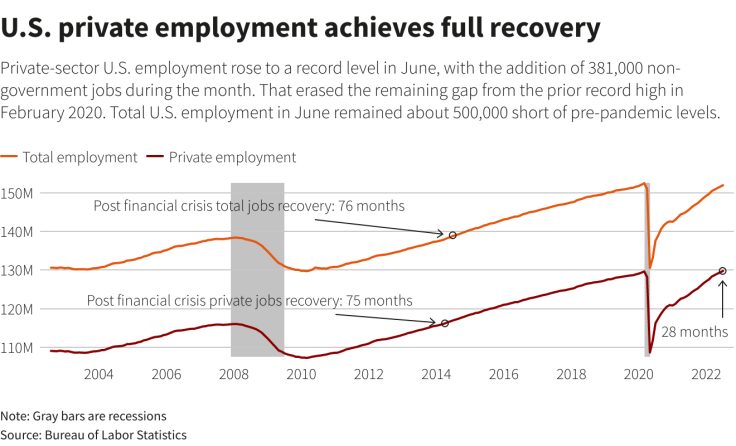

GRAPHIC: U.S. private employment set to achieve full recovery

On the downside, personal consumption data for May, released last week, showed spending and disposable income dropped on an inflation-adjusted basis. That sparked a host of gloomy forecasts for June, and increasing speculation that a downturn is coming soon, if it is not here already.

The weeks ahead are likely to include pitched debate about the real health of the economy. Whether the U.S. is headed for a recession or already in one is a growing concern for corporate chief executives and their employees, the Federal Reserve, and the administration of President Joe Biden.

IS A RECESSION ALWAYS TWO CONSECUTIVE Qs OF FALLING GDP?

Usually, but not always.

For example, GDP in 2001, after revisions, fell in the first three months of the year, rebounded in the next three months and declined again in the fall.

Even though there were not two consecutive quarters of declining GDP, the situation was a defined as a recession, because employment and industrial production were falling.

GRAPHIC: Two quarters of decline?

The COVID-19 pandemic recession only lasted two months, economists determined afterward, from March to April 2020, even though the steep drop in economic activity over those weeks meant GDP shrank overall in both the first and second quarters of the year.

WHO DECIDES, AND HOW?

In the United States the official call is made by a panel of economists convened by the National Bureau of Economic Research, and sometimes comes a year or more after the fact.

The private non-profit research group defines https://www.nber.org/business-cycle-dating-procedure-frequently-asked-questions#:~:text=A%3A%20The%20NBER's%20traditional%20definition,more%20than%20a%20few%20months recession as a "significant decline in economic activity that is spread across the economy and that lasts more than a few months."

The panel concentrates on things like jobs and industrial output that are measured monthly, not quarterly like GDP. It examines the depth of any changes, how long declines seem to be lasting, and how broadly any trouble is spread.

There are tradeoffs.

In the pandemic, for example, the depth of the job loss, in excess of 20 million positions, offset the fact that growth resumed quickly, leading the group to officially call the situation a recession in early June, before the end of the second quarter.

While each of three criteria - depth, diffusion, and even duration -- "needs to be met individually to some degree, extreme conditions revealed by one criterion may partially offset weaker indications from another," the group says.

SO ARE WE IN A RECESSION NOW?

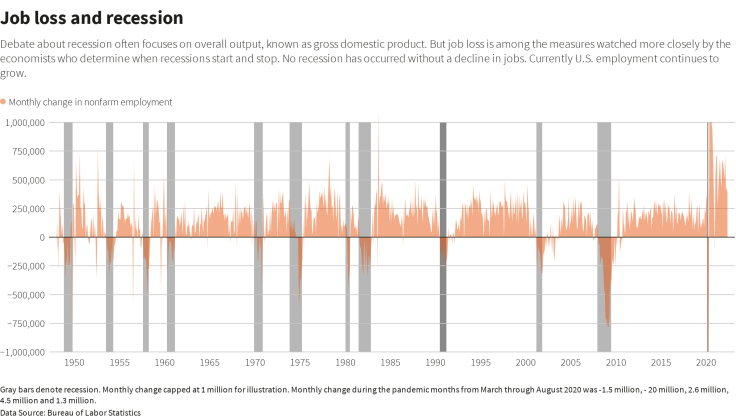

Almost certainly not. While the "two quarter rule" has caveats and exceptions, there has never been a recession declared without a loss of employment. Jobs are being added in the U.S. by hundreds of thousands monthly.

GRAPHIC: Job loss and recession

The pace will likely slow, but there would need to be a sharp reversal for the current path of job growth to turn into one that looks like recession.

Industrial production, another factor that figured prominently in declaring the 2001 recession, has also been rising steadily, at least through May.

Since 1950 the United States has not experienced a two quarters-in-a-row contraction in GDP that was not utimately associated with a recession, which could make the current "are we or aren't we" debate even more contentious.

WHAT IS THE SAHM RULE?

One criticism of the NBER's role as a recession arbiter is that its members take their time in order to avoid reacting to changes in jobs, production or other data that prove temporary. A closer to real-time recession indicator, called the Sahm rule after former Fed economist Claudia Sahm, is based on the unemployment rate.

It states that when the 3-month rolling average of the unemployment rate rises a half a percentage point from its low over the prior 12 months, the economy has entered a recession.

The Sahm rule shows no sign of a U.S. downturn. Instead, the unemployment rate has been below 4% and falling or stable since January. WHY DOES THE R-WORD MATTER?

Discussion of a recession, and predictions that the U.S. economy is headed into one, can have an impact on what happens next. CEOs, investors and everyday consumers make decisions on where and how to spend money based on how they think sales, profits and employment conditions will evolve.

Economist Robert Shiller predicted in June that there was a "good chance" the U.S. would experience a recession as a result of a "self-fulfilling prophecy" as consumers and companies prepare for the worst. "The fear can lead to the actuality," he told Bloomberg.

WHAT IS A 'SHALLOW RECESSION?'

Recessions come in many shapes. They can be deep but brief, like the pandemic recession which sent the unemployment rate briefly to 14.7%. They can be deep and scarring, like the Great Recession or the Depression in the 1930s, taking years for the job market to regain lost ground.

Economists and analysts have recently flagged the possibility that the next U.S. recession may be a mild one. Even the shortest and weakest recessions have trimmed payroll jobs by more than 1%, which would currently amount to more than a million and a half people.

WHAT IS A GROWTH RECESSION? Another idea discussed by some economists and analysts is a "growth recession," in which economic growth slows below the U.S. long-term growth trend of 1.5 to 2 percent annually, while unemployment increases but not by a lot. This is the scenario mapped out by some Fed policymakers as the best case outcome of recent interest rate increases.

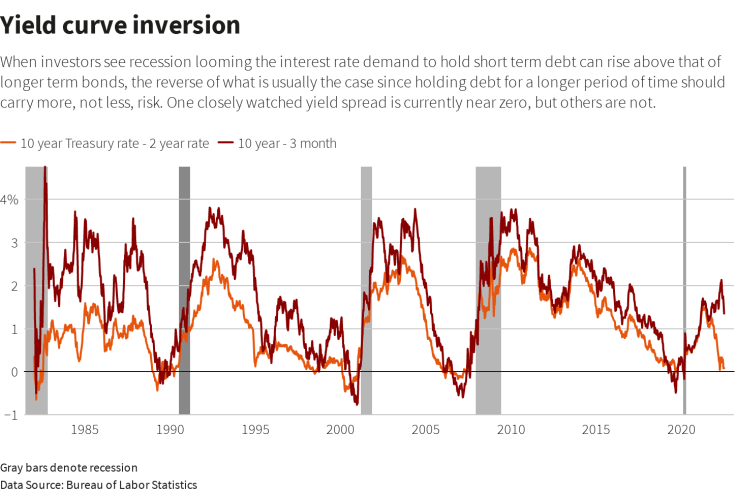

WHAT'S THE INVERTED YIELD CURVE LINK?

When the market rate for short-term borrowing exceeds that for a longer-term loan, it is known as an inverted yield curve, and seen as a harbinger of a recession.

Historically at least some part of the yield curve has inverted before every recent recession, and alarm bells started ringing when that happened on June 13.

Research from the Federal Reserve argues that the most widely followed yield-curve measure, the gap between yields on the two-year and the 10-year Treasury notes, doesn't actually predict much of anything; a better

gauge is the gap between three-month and 18-month rates, which has not inverted.

GRAPHIC: Yield curve inversion

WHAT IS THE BEAR MARKET LINK TO RECESSION?

The recent steep stock sell-off has also set off alarms. Nine of 12 bear markets, or drops of more than 20%, that have occurred since 1948 have been accompanied by recessions, according to investment research firm CFRA.

© Copyright Thomson Reuters 2024. All rights reserved.

- MOST POPULAR IN Economy & Markets